With advances in technology and new ways to utilize data, some companies have sprouted up to create different ways to sell your property.

Basically, they utilize automated valuation models (AVMs) to make quick offers on homes, allowing

them to close in a much faster than typical timeframe, and then resell them.

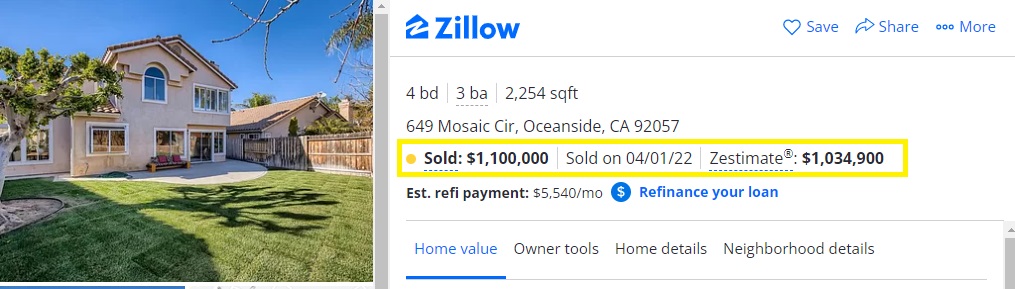

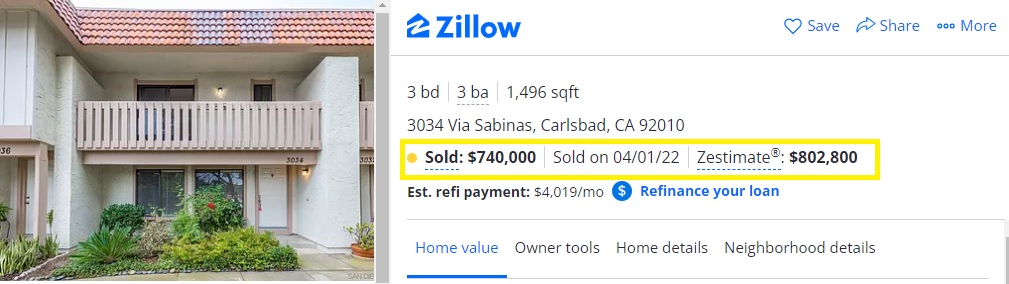

From a seller’s standpoint, it can eliminate some hassle and uncertainty, but with high “transaction fees” ranging from 7% to 14%, and the likelihood that they will sell the home for more than they paid you for it, you are simply exchanging that smooth and quick transaction for a portion of your equity.

Companies that offer this kind of service are only in limited markets across the country right now. They operate by having homeowners fill out a short questionnaire with information on their home. They feed that data into their AVM, which kicks back an offer price. They make the homeowner a cash offer to close in a short timeframe (typically about a week) and specify what the fee will be to proceed through to closing. Once they own the home, they will repair and spruce it up, and list it for sale on the open market.

It may be tempting to consider such an offer, but keep in mind that this is a straight numbers play. They are determining a price that allows them the room to cover the costs of the transactions as well as the repairs, while still making some profit. Their profit will either come from the fee you’ve paid or from acquiring your home at a below market price – although it could possibly be a combination of the two.

n analysis on one company’s transactions showed they were selling homes at an average 5.5% appreciation, on top of their transaction fee. That’s a lot of money to leave on the table for a little convenience.

There are other companies beginning to test alternative listing models as well, utilizing technology and AVMs to make ‘instant offers’ on homes, or to help buyers acquire and move into their next home before selling their current one. As always, it’s important to read the fine print and understand what you are agreeing to before using the service.

Hi folks,

If you are going to be selling your home in the near future or are just curious about its value in today’s market, give me a call or use the button below. I will email you a comprehensive market analysis of your home. There is no obligation on your part and it is totally free.

My phone number is 760.476.9560.

What is my Home Worth

Not ready to move yet but want to keep an eye on your homes value, I have a monthly update that is customized to your home and neighborhood. Click the link below to see what is included in the report and to sign up:

Monthly Update